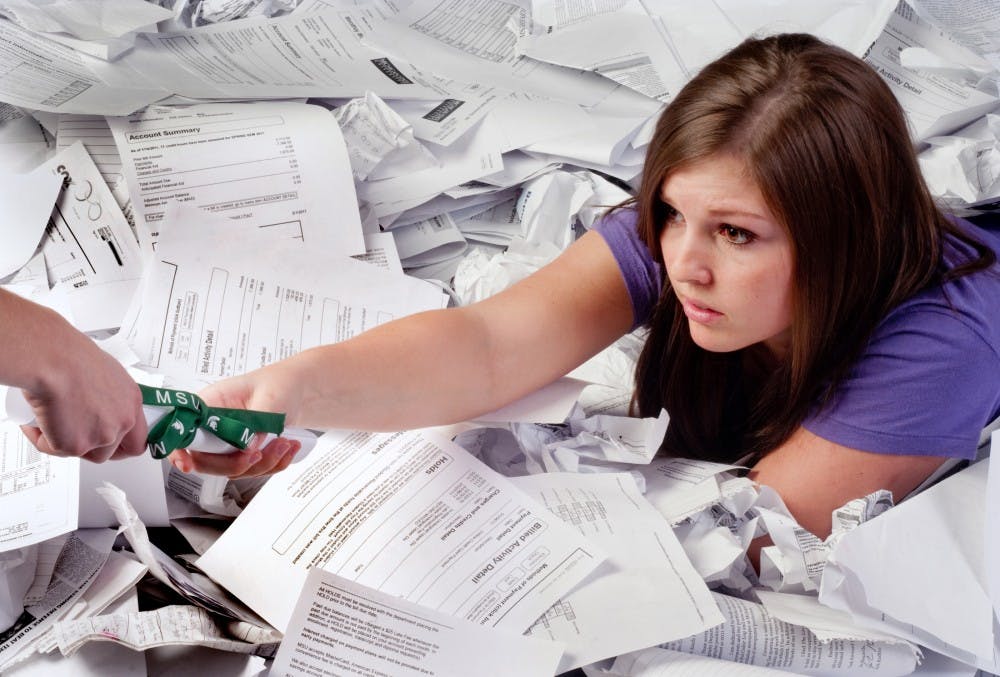

McLean graduated from MSU in August 2010 with a degree in accounting and $65,000 in student loans.

Although his family makes “really good money,” they thought he should pay for college on his own, he said. At the time, they didn’t realize how much more expensive a university education had become since their time at school.

“They had no idea that I had to pull out so many loans,” McLean said.

Loan landslide

McLean’s story is on the extreme end compared to the average American university student, but college students are borrowing at an increasing rate, said Rich Williams, a higher education advocate at U.S. Public Interest Research Groups, or U.S. PIRG, a network of state-based student advocacy organizations.

In 1998, one-third of college students took out a loan during their time in college and graduated with an average of $12,000 worth of debt, he said.

By 2008, that number jumped to two-thirds of college students taking out an average of nearly $24,000.

“Many more students are borrowing and many more students are borrowing more,” Williams said.

MSU has seen the growth in borrowing as well, partially because of the cancellation of state grants and programs, including the Michigan Promise Scholarship, said Val Meyers, associate director of the Office of Financial Aid.

Although federal grant money is growing, it’s not rising as fast as the rising cost of tuition, and MSU is continuing to pump more money into its own financial aid programs to fight that problem, she said.

“We’re staying even (with increasing tuition costs), the federal government’s not and the state is not,” Meyers said. “More and more of that gap will be filled by loans.”

Last year, about 24,000 students took out at least one federal student loan through the Office of Financial Aid, a little more than 50 percent of eligible students, Meyers said.

Of students that graduated in 2009 who had borrowed, most were left with between $10,000 to $19,999 to pay off — but a little less than 10 percent owed $30,000 or more.

“It’s really hard to judge how it affects an average student and an average family,” Meyers said. “For students with high need, the borrowing is getting a little bit out of control and we’re very concerned about that.”

Federal dollars

McLean was able to get about $9,000 in federal student loans by filling out the Free Application for Federal Student Aid, or FAFSA, he said. The remainder of his debt accrued from private loans with much higher interest rates.

One private loan he took out for $3,000 his freshman year accumulated to $12,000 in debt when he graduated five years later, he said.

“The interest just kept building and building and building,” said McLean, who currently is paying a total of about $250 each month in loan payments on two different loans. “It’s ugly.”

About 28 percent of students do not complete the FAFSA in the first place, said Patricia Nash Christel, a spokeswoman for Sallie Mae, a company that provides private loans and is one of four servicers for federal student loans.

Of those students, about half said they did not think they would qualify for federal aid or were unaware of the form, she said.

“Virtually every U.S. citizen would qualify for some type of financial aid, whether it’s a grant or a federal student loan,” Christel said. “It may not be the top of your list for a fun activity, but it’s certainly time well spent in making sure you are aware of every resource.”

Support student media!

Please consider donating to The State News and help fund the future of journalism.

In fiscal year 2010, the federal government distributed $101.5 billion in loans to students, said Sara Gast, spokeswoman for the Department of Education.

Sallie Mae’s private student loans have interest rates ranging from 2.88 to 10.25 percent, but they offer a Smart Option Student Loan that allows students to pay the interest on the loans while they’re still in school, Christel said.

“It can save between 30 and 50 percent over the life of the loan, just by paying a little bit in school,” Christel said.

Advertising sophomore John Reid has taken out several federal loans through the Office of Financial Aid, but he has a goal of paying them off soon after graduation.

“A lot of people get out there and get their debt right away and pay their student loans off for 30 years,” Reid said. “I want to have them paid off by the time I’m 30.”

Human resource management freshman Emily Kasper also said she’s felt very “money-conscious” during her first two semesters at MSU.

She currently has taken about $5,000 in federal loans and her parents are helping her pay about half of her college expenses. The lack of merit-based scholarships she was able to find on campus was frustrating, she said.

“It kind of scared me having that much money in my name in debt,” Kasper said. “I just don’t like the idea of being unnecessarily in debt when I’m taking classes that are really prerequisites.”

In perspective

With the difficult economic times, parents and students overwhelmingly are seeing the value in a college education, according to a 2010 “How America Pays for College” survey by Sallie Mae and Gallup, Christel said. Families are digging deeper to invest in what they value, she said.

Meyers said it usually is not possible for a student to pay their entire tuition off of federal loan money, but MSU has been putting more funds into assistance grants, such as the Spartan Advantage Program.

“A lot of families in Michigan are having a difficult time because of the economy,” she said. “If you’re an autoworker and you lost your job, the last thing you want to worry is whether you can keep your son or daughter in school.”

Plus, most loans offer several different repayment options.

The standard length is 10 years, but the government recently introduced an Income Contingent Repayment Plan with loan payments tailored so they do not exceed more than 15 percent of a graduate’s income, she said.

For McLean, his loans will be paid off faster than he anticipated because he’s decided to join the Army. The military will pay for his government loans and he won’t have to pay money out-of-pocket for housing, food or clothes, he said.

“In about two and a half years, I will be able to pay all my loans off,” McLean said.

And although he said he had good money management skills heading into college, McLean said having to take out loans himself has made him realize the value of his university education.

“They made me appreciate school more,” McLean said.

Discussion

Share and discuss “The debt dilemma” on social media.